Earth SciencesCommunications Earth & Environment

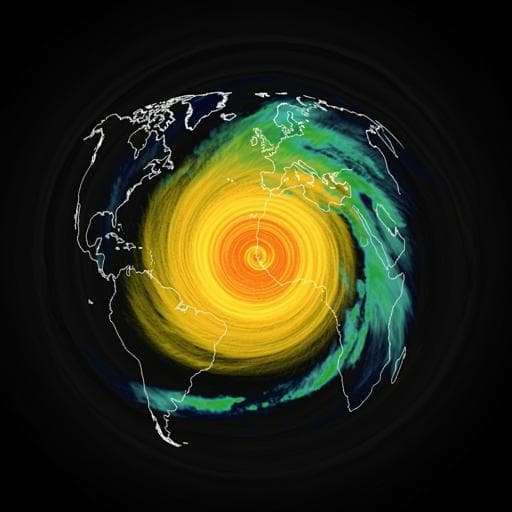

Increase in insurance losses caused by North Atlantic hurricanes in a warmer climate

F. Comola, B. Märtl, et al.

Discover the startling findings of research conducted by Francesco Comola, Bernhard Märtl, Hilary Paul, Christian Bruns, and Klaus Sapelza, which projects significant increases in insurance losses from North Atlantic hurricanes due to climate change. Learn how warming scenarios could reshape the landscape of hurricane-related financial risks, with expected losses potentially escalating by up to 30%.

Related Publications

Explore these studies to deepen your understanding

Adjacent work that informs or extends this paper's methodology and findings.

Earth Sciences

Wide range of possible trajectories of North Atlantic climate in a warming world

Q. Gu, M. Gervais, et al.

Earth Sciences

Europe faces up to tenfold increase in extreme fires in a warming climate

S. E. Garroussi, F. D. Giuseppe, et al.

Environmental Studies and Forestry

High-ambition climate action in all sectors can achieve a 65% greenhouse gas emissions reduction in the United States by 2035

A. Zhao, K. T. V. O’keefe, et al.

Medicine and Health

Body composition, physical capacity, and immuno-metabolic profile in community-acquired pneumonia caused by COVID-19, influenza, and bacteria: a prospective cohort study

C. K. Ryrsø, A. M. Dungu, et al.